Student Loan Repayment 2025: Income-Driven Analysis

Anúncios

Effectively managing student loan repayment in 2025 hinges on understanding various income-driven repayment plans, which offer crucial flexibility based on your financial situation and future earning potential.

Anúncios

Navigating the complexities of student loan debt can feel overwhelming, but understanding your student loan repayment options for 2025: a data-driven analysis of income-driven plans is crucial for financial stability. As economic landscapes shift and educational costs continue to rise, knowing the best approach to manage your student loans is more important than ever. This guide will help you decipher the various paths available, particularly focusing on income-driven repayment plans, to empower you with the knowledge needed to make informed decisions.

The Evolving Landscape of Student Loan Repayment in 2025

The world of student loan repayment is not static; it constantly evolves with new policies, economic shifts, and legislative changes. For 2025, borrowers need to be particularly aware of these dynamics to optimize their repayment strategies. Understanding the current context is the first step toward making effective decisions about your financial future.

Anúncios

The economic climate, including inflation rates and employment trends, directly impacts borrowers’ ability to repay their loans. Moreover, federal policies regarding interest rates, loan forgiveness programs, and eligibility criteria for various repayment plans are subject to adjustments. Staying informed about these changes is paramount to avoiding pitfalls and maximizing benefits.

Key Policy Updates and Economic Factors

Several factors are shaping the student loan environment for 2025. These include potential changes in federal interest rate caps, adjustments to poverty guidelines used in income-driven repayment calculations, and the ongoing impact of post-pandemic economic recovery. These elements collectively determine the feasibility and attractiveness of different repayment avenues.

- Federal Interest Rate Forecasts: Anticipate fluctuations in federal interest rates, which can affect overall loan costs.

- Poverty Guideline Adjustments: Annual updates to federal poverty guidelines influence payment calculations for income-driven plans.

- Employment Market Trends: A strong job market can improve repayment capacity, while a weaker one might necessitate more flexible repayment options.

Furthermore, technological advancements are playing a role in how borrowers interact with their loan servicers and access information. Digital platforms and personalized financial tools are becoming increasingly sophisticated, offering new ways to track loans, calculate payments, and explore different options. Leveraging these resources can significantly streamline the repayment process.

In conclusion, the 2025 student loan repayment landscape requires proactive engagement. Borrowers must remain vigilant about policy updates and economic indicators, as these external factors will heavily influence the most advantageous repayment strategies. Being well-informed is the strongest defense against financial strain and the best path toward successful loan management.

Deciphering Income-Driven Repayment (IDR) Plans

Income-Driven Repayment (IDR) plans are a cornerstone of federal student loan management, designed to make monthly payments more affordable by basing them on a borrower’s income and family size. These plans are particularly vital for those with high loan balances relative to their earnings, providing a financial safety net and a clear path toward eventual loan forgiveness.

The core principle behind IDR plans is to prevent default by ensuring that payments are manageable. Instead of a fixed payment amount that might strain a tight budget, IDR plans adjust payments annually, reflecting changes in your financial situation. This flexibility is a significant advantage for many borrowers.

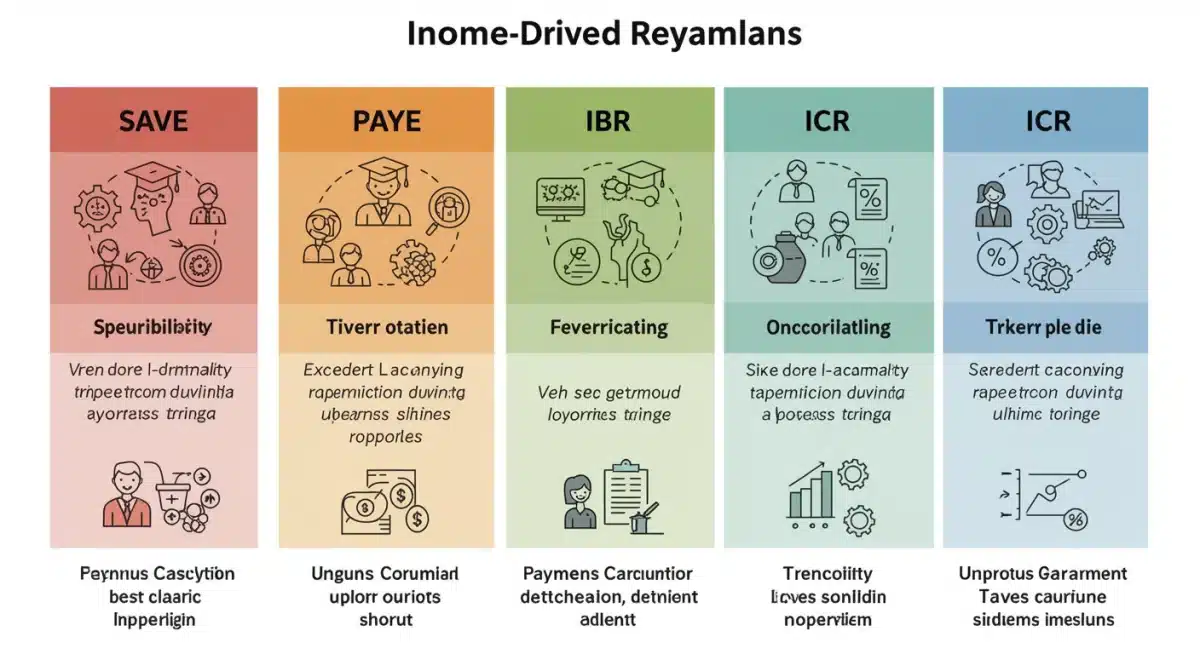

Exploring the Main IDR Options: SAVE, PAYE, IBR, and ICR

As of 2025, several distinct IDR plans are available, each with its own nuances regarding eligibility, payment calculations, and forgiveness timelines. Understanding these differences is critical for selecting the plan that best suits your individual circumstances.

- SAVE Plan (Saving on a Valuable Education): This is the newest IDR plan, offering some of the most generous terms, including lower monthly payments for many borrowers and a provision that prevents your balance from growing due to unpaid interest.

- PAYE Plan (Pay As You Earn): Payments are generally 10% of your discretionary income, and loans are forgiven after 20 years of payments. This plan often has lower payments than IBR.

- IBR Plan (Income-Based Repayment): Payments are either 10% or 15% of your discretionary income, depending on when you took out your loans, with forgiveness after 20 or 25 years.

- ICR Plan (Income-Contingent Repayment): This is the oldest IDR plan, with payments calculated as the lesser of 20% of your discretionary income or what you would pay on a fixed 12-year payment plan, adjusted for income. Forgiveness occurs after 25 years.

Choosing the right IDR plan involves a careful comparison of these features against your current income, projected future earnings, family size, and total loan amount. It’s not a one-size-fits-all decision, and what works for one borrower might not be ideal for another. Many borrowers find that the SAVE plan offers the most advantageous terms due to its interest subsidy and potentially lower payments.

In summary, IDR plans offer essential flexibility and protection for federal student loan borrowers. By understanding the specific characteristics of the SAVE, PAYE, IBR, and ICR plans, individuals can strategically manage their debt, potentially reducing their monthly burden and working towards ultimate loan forgiveness. Regular re-evaluation of your plan is also crucial as your financial situation evolves.

Data-Driven Insights: Who Benefits Most from IDR Plans?

A data-driven analysis reveals that certain borrower demographics and financial situations are particularly well-suited for Income-Driven Repayment (IDR) plans. Understanding these patterns can help individuals assess whether an IDR plan is their most advantageous option. This isn’t just about anecdotes; it’s about leveraging aggregate data to identify optimal strategies.

Research consistently shows that borrowers with lower incomes relative to their debt burden, especially those in public service or non-profit sectors, tend to benefit significantly from IDR plans due to the potential for Public Service Loan Forgiveness (PSLF) after 10 years of qualifying payments. However, the benefits extend beyond PSLF-eligible professions.

Statistical Trends and Ideal Candidate Profiles

Recent studies and government data highlight specific scenarios where IDR plans provide the most substantial relief. These include individuals pursuing careers with modest starting salaries but high educational debt, or those who experience temporary periods of unemployment or underemployment.

- High Debt-to-Income Ratio: Borrowers whose total student loan debt significantly exceeds their annual income are prime candidates for IDR, as it caps payments at an affordable percentage of their discretionary income.

- Public Service Employment: Those working for government entities or qualifying non-profits can achieve loan forgiveness much faster (10 years) under IDR plans, especially when combined with PSLF.

- Fluctuating Income: Individuals with variable incomes, such as freelancers or those in commission-based roles, find IDR plans beneficial because payments adjust with their earnings.

- Graduate Degree Holders with High Debt: While often having higher earning potential, graduate students frequently accumulate substantial debt, making IDR a crucial tool for managing initial repayment periods.

The data also suggests that younger borrowers, often facing entry-level salaries, can greatly benefit from the initial lower payments offered by IDR plans. This allows them to allocate more resources to other financial goals, such as saving for a down payment or building an emergency fund, without defaulting on their student loans.

Ultimately, a data-driven approach to IDR analysis reveals that these plans are not just for those in dire financial straits but can be a strategic tool for a wide range of borrowers. By understanding the statistical likelihood of benefit, individuals can make more informed choices about their repayment journey, aligning their loan strategy with their broader financial objectives and career aspirations.

Comparing IDR to Standard Repayment Plans

While Income-Driven Repayment (IDR) plans offer significant flexibility, it’s essential to compare them against traditional standard repayment plans to fully grasp their advantages and disadvantages. Standard plans often involve higher monthly payments but can result in less interest paid over the life of the loan. The choice between these two broad categories depends heavily on individual financial circumstances and priorities.

Standard repayment plans typically amortize the loan over a fixed period, usually 10 years, with equal monthly payments. This predictable structure works well for borrowers with stable, higher incomes who can comfortably afford the payments and wish to pay off their debt quickly.

Key Differences in Payment Structure and Long-Term Costs

The fundamental difference lies in how monthly payments are calculated and the overall duration of the repayment period. IDR plans prioritize affordability based on income, potentially extending the repayment term and leading to more interest paid over time, though they often culminate in loan forgiveness.

- Monthly Payment Calculation: Standard plans use a fixed principal and interest calculation. IDR plans base payments on discretionary income and family size.

- Repayment Term: Standard plans are typically 10 years. IDR plans can extend to 20 or 25 years, or even 10 years for PSLF-eligible borrowers.

- Total Interest Paid: Generally, standard plans result in less interest paid overall due to the shorter term. IDR plans, especially those with low payments, can accumulate more interest before forgiveness.

- Loan Forgiveness: Standard plans do not offer loan forgiveness. IDR plans offer forgiveness of remaining balances after the repayment term, provided all conditions are met.

For borrowers prioritizing lower monthly payments and the potential for forgiveness, IDR plans are often the preferred choice. This is especially true for those facing financial hardship or pursuing careers that qualify for PSLF. However, if your goal is to minimize the total amount paid and you have the income to support higher monthly installments, a standard repayment plan might be more cost-effective in the long run.

In conclusion, the decision between IDR and standard repayment plans is a personalized one. It requires a careful evaluation of your current financial health, future earning potential, and long-term financial goals. While IDR offers crucial flexibility and a path to forgiveness, standard plans can be more economical for those who can manage the higher monthly payments and wish to pay off their debt sooner. It’s not about one being inherently better, but about choosing the plan that aligns best with your unique situation.

The Impact of the SAVE Plan for 2025 Borrowers

The Saving on a Valuable Education (SAVE) Plan, introduced as an enhancement to the Revised Pay As You Earn (REPAYE) plan, represents a significant shift in federal student loan repayment options for 2025. It offers potentially the most generous terms for many borrowers, aiming to make monthly payments more affordable and prevent loan balances from growing due to unpaid interest. Understanding its specific features is crucial for anyone considering an IDR plan.

The SAVE Plan is designed to provide greater financial relief, particularly for low- and middle-income borrowers. Its structure addresses some of the common criticisms of previous IDR plans, making it a more accessible and beneficial option for a broader range of individuals.

Key Features and Advantages of the SAVE Plan

The SAVE Plan introduces several innovative elements that set it apart from other IDR options. These features are specifically tailored to reduce financial burden and offer a clearer path to debt freedom for eligible borrowers.

- Lower Monthly Payments: For undergraduate loans, payments are calculated as 5% of discretionary income, down from 10% in other plans. Payments for graduate loans remain at 10%, or a weighted average if you have both.

- Interest Subsidy: If your calculated monthly payment doesn’t cover the accrued interest, the government covers the remaining interest. This prevents your loan balance from increasing, even if you’re paying $0 monthly.

- Higher Income Exemption: The amount of income considered discretionary is increased from 150% to 225% of the federal poverty line, meaning more of your income is protected and not factored into your payment calculation.

- Shorter Forgiveness Timelines for Small Balances: Borrowers with original principal balances of $12,000 or less may qualify for forgiveness after as few as 10 years of payments.

These features collectively make the SAVE Plan a powerful tool for managing student loan debt. The interest subsidy, in particular, is a game-changer, as it eliminates the disheartening experience of seeing your loan balance grow even while making payments. This aspect alone can provide significant psychological and financial relief.

For 2025 borrowers, especially those with undergraduate loans or modest incomes, the SAVE Plan should be a primary consideration. Its benefits are designed to alleviate financial stress, accelerate the path to forgiveness for some, and provide a more stable repayment journey overall. Regularly checking your eligibility and comparing it against other plans is a smart financial move.

Navigating the Application and Recertification Process

Once you’ve identified the most suitable Income-Driven Repayment (IDR) plan for your situation in 2025, the next critical step is understanding the application and, crucially, the annual recertification process. These administrative tasks are vital to enrolling in and maintaining your IDR benefits. Missing deadlines or making errors can lead to higher payments or even removal from the plan.

The application process typically involves providing information about your income and family size, which your loan servicer uses to calculate your monthly payment. This initial step is relatively straightforward, but the ongoing requirement for annual recertification is where many borrowers encounter challenges.

Step-by-Step Guide to Applying and Recertifying

Staying organized and proactive is key to successfully navigating the IDR application and recertification. Familiarize yourself with the necessary documents and timelines to avoid any interruptions in your payment plan.

- Initial Application: You can apply for an IDR plan through your loan servicer’s website or by completing the Income-Driven Repayment Plan Request form on the Federal Student Aid website. You’ll need your tax returns or other income documentation and information about your family size.

- Automatic Recertification: Whenever possible, opt-in for automatic recertification. This allows the Department of Education to access your tax information directly from the IRS, simplifying the process and reducing the chance of missing deadlines.

- Manual Recertification: If you don’t opt for automatic recertification, you will need to manually submit updated income and family size information annually. Your loan servicer will send reminders, but it’s your responsibility to ensure the information is submitted on time, usually 30-90 days before your annual recertification date.

- Documentation: Be prepared to provide recent pay stubs, tax returns, or a letter from your employer verifying your income. For family size, you’ll typically attest to the number of dependents you support.

The consequences of failing to recertify on time can be significant. Your monthly payments may revert to the higher standard repayment amount, and any unpaid interest that was previously subsidized might be capitalized, meaning it’s added to your principal balance, causing your loan to grow. Therefore, treating recertification with the same importance as the initial application is essential.

In conclusion, successfully managing an IDR plan extends beyond selecting the right option; it encompasses diligent adherence to the application and annual recertification requirements. By understanding the process, utilizing available tools like automatic recertification, and keeping track of deadlines, borrowers can ensure they continue to receive the benefits of their chosen IDR plan, maintaining affordable payments and progressing toward loan forgiveness.

Strategic Considerations and Future Planning for Student Loans

Beyond simply choosing a repayment plan, strategic considerations and future planning are paramount for long-term student loan success in 2025. This involves more than just making monthly payments; it encompasses understanding the interplay between your loans, career trajectory, and broader financial goals. A holistic approach can transform student loan management from a burden into a manageable part of your financial life.

Effective planning requires anticipating future income changes, understanding the implications of life events like marriage or starting a family, and exploring additional strategies such as refinancing or consolidation. It’s about building a roadmap that adapts to your evolving circumstances.

Refinancing, Consolidation, and Other Advanced Strategies

For some borrowers, particularly those with strong credit and stable income, exploring options beyond federal IDR plans can lead to further savings or simplified management. However, it’s crucial to understand the trade-offs involved.

- Federal Loan Consolidation: This combines multiple federal loans into a single Direct Consolidation Loan with a new fixed interest rate (a weighted average of the original rates). It can simplify payments and sometimes open doors to additional IDR plans or PSLF eligibility, but it doesn’t necessarily lower your interest rate.

- Private Student Loan Refinancing: This involves taking out a new loan from a private lender to pay off existing federal or private student loans. It can potentially lower your interest rate or monthly payment, but you lose federal loan benefits like IDR plans, forbearance, deferment, and access to forgiveness programs. This is a significant trade-off to consider.

- Aggressive Repayment: For those who can afford it, making extra payments or paying more than the minimum can significantly reduce the total interest paid and accelerate loan payoff.

- Emergency Fund and Budgeting: Maintaining a robust emergency fund and a detailed budget are fundamental to managing student loans, providing a buffer against unexpected financial setbacks and ensuring you can consistently meet your obligations.

Considering your career path is also vital. If you anticipate working in public service, focusing on PSLF-eligible IDR plans is a clear strategy. If you foresee a high-earning career in the private sector, the benefits of refinancing for a lower interest rate might outweigh the loss of federal protections. These decisions are highly personal and should be based on a thorough assessment of your individual circumstances.

In conclusion, strategic student loan management in 2025 goes beyond merely selecting a repayment plan. It involves a continuous process of evaluation, adaptation, and proactive decision-making. By combining a solid understanding of IDR plans with considerations for consolidation, refinancing, and sound financial habits, borrowers can effectively navigate their student loan journey and achieve long-term financial well-being.

| Key Aspect | Brief Description |

|---|---|

| SAVE Plan | Newest IDR plan with lower undergraduate payments (5% discretionary income) and interest subsidy. |

| IDR Eligibility | Primarily for federal loans; based on income and family size; requiring annual recertification. |

| Loan Forgiveness | Available after 10-25 years of qualifying payments under IDR, or 10 years for PSLF. |

| Recertification | Annual process to update income and family size; crucial for maintaining IDR benefits. |

Frequently Asked Questions About Student Loan Repayment in 2025

In 2025, the main income-driven repayment (IDR) plans for federal student loans include the SAVE Plan, Pay As You Earn (PAYE), Income-Based Repayment (IBR), and Income-Contingent Repayment (ICR). Each plan offers different payment calculations and forgiveness timelines based on your income and family size.

The SAVE Plan offers several key benefits, including lower monthly payments for undergraduate loans (5% of discretionary income), an interest subsidy that prevents your loan balance from growing due to unpaid interest, and a higher income exemption, making payments more affordable for many borrowers.

Ideal candidates for IDR plans typically have a high debt-to-income ratio, work in public service, have fluctuating incomes, or hold graduate degrees with substantial debt. These plans provide crucial flexibility and a path to forgiveness for those who might struggle with standard payments.

Annual recertification is critical for maintaining your IDR benefits. It requires you to update your income and family size information so your loan servicer can adjust your payments. Failing to recertify on time can lead to higher monthly payments and potential capitalization of unpaid interest.

Refinancing federal student loans with a private lender can potentially lower your interest rate or monthly payment. However, it means losing valuable federal benefits like access to IDR plans, forbearance, deferment, and loan forgiveness programs. This decision requires careful consideration of the trade-offs.

Conclusion

The landscape of student loan repayment in 2025, particularly concerning income-driven plans, presents both challenges and opportunities for borrowers. A thorough understanding of options like the SAVE, PAYE, IBR, and ICR plans, coupled with strategic financial planning, is essential for navigating this complex terrain. By leveraging data-driven insights, proactively managing the application and recertification processes, and continuously evaluating personal financial circumstances, borrowers can make informed decisions that lead to sustainable and ultimately successful student loan management. Staying informed and adaptable is key to achieving financial freedom from student debt.