The 2026 Open Enrollment Period for Health Insurance: Don’t Miss the December 15th Deadline for New Plans (TIME-SENSITIVE)

As the calendar pages turn, a critical period approaches for millions of Americans: the 2026 Open Enrollment Period for health insurance. This annual window is your opportunity to secure health coverage for the upcoming year, adjust your existing plan, or explore new options that better fit your evolving needs and budget. Missing this period can have significant consequences, potentially leaving you without vital coverage or locked into a plan that no longer serves you. The most crucial date to mark on your calendar, especially if you’re seeking new coverage starting January 1, 2026, is December 15th. This isn’t just another date; it’s the 2026 Health Enrollment Deadline for timely coverage, a gateway to peace of mind and access to essential healthcare services.

Anúncios

Navigating the complexities of health insurance can feel daunting. With various plans, metal tiers, deductibles, co-pays, and networks, understanding your choices and making an informed decision requires careful consideration. This comprehensive guide is designed to demystify the 2026 Open Enrollment Period, providing you with all the essential information you need to confidently select the best health insurance plan for yourself and your family. We’ll cover everything from key dates and eligibility to understanding plan types, comparing costs, and utilizing available financial assistance. Our primary goal is to ensure you are well-prepared to meet the December 15th deadline and secure the coverage you deserve.

Understanding the 2026 Open Enrollment Period: What You Need to Know

The Open Enrollment Period (OEP) is the designated time each year when individuals and families can enroll in a health insurance plan through the Health Insurance Marketplace (also known as the exchange) or directly from an insurance company. Outside of this period, you can only enroll or change plans if you qualify for a Special Enrollment Period (SEP), triggered by specific life events like marriage, birth of a child, loss of other coverage, or moving to a new area. Therefore, leveraging the OEP is paramount.

Anúncios

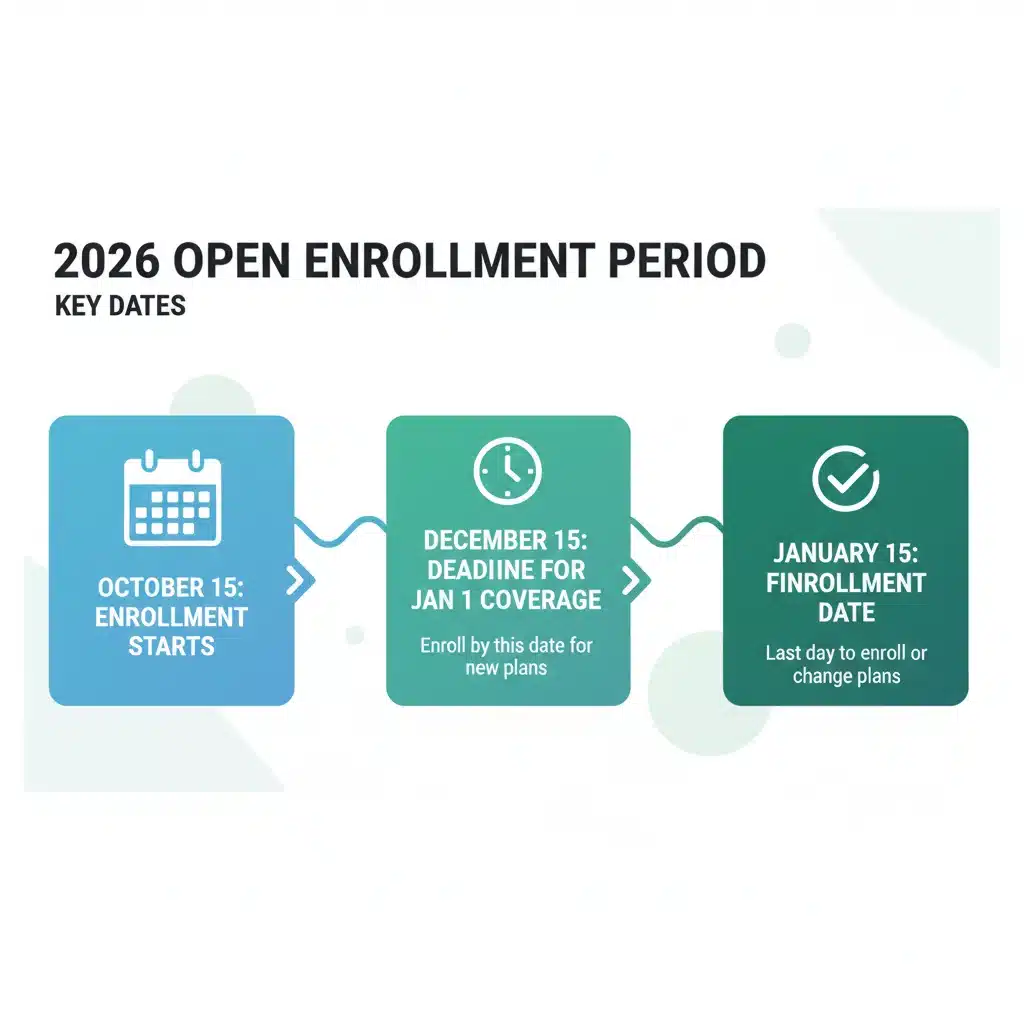

Key Dates for the 2026 Open Enrollment

While the exact start and end dates for the entire 2026 Open Enrollment Period can vary slightly by state, the most critical date for federal marketplaces and many state-based exchanges remains consistent: December 15th.

- November 1, 2025: This is typically when the 2026 Open Enrollment Period officially begins. At this point, you can start exploring plans, comparing options, and submitting applications for coverage starting January 1, 2026.

- December 15, 2025: This is the firm 2026 Health Enrollment Deadline if you want your new health insurance coverage to begin on January 1, 2026. If you enroll after this date but before the final enrollment deadline, your coverage start date will be later.

- January 15, 2026: This is usually the final day of the Open Enrollment Period for federal marketplaces. If you enroll between December 16th and January 15th, your coverage will typically begin on February 1, 2026. However, some state-based marketplaces may have extended deadlines, so it’s vital to check your specific state’s rules.

Given the importance of continuous coverage, aiming to complete your enrollment by the December 15th deadline is highly recommended. This ensures there’s no gap in your health protection as you transition into the new year.

Why the December 15th Deadline is Crucial for 2026 Health Enrollment

The significance of the December 15th deadline cannot be overstated. For many, this date determines whether they will have health insurance coverage from the very first day of 2026. Imagine facing an unexpected medical emergency on January 2nd without coverage because you missed the priority enrollment window. The financial implications could be devastating. By enrolling by December 15th, you guarantee that your new or updated plan will be active when the new year begins, providing seamless protection for you and your loved ones.

Furthermore, delaying your enrollment beyond this date means your coverage might not kick in until February 1st or even March 1st, depending on when you complete the process. This gap in coverage exposes you to financial risk for any healthcare needs that arise in the interim. Therefore, making timely decisions during the 2026 Open Enrollment Period is not just about compliance; it’s about safeguarding your health and financial well-being.

Who Needs to Act During the 2026 Open Enrollment Period?

The 2026 Open Enrollment Period is relevant to a broad spectrum of individuals and families:

- Currently Uninsured Individuals: If you don’t have health insurance, this is your primary opportunity to get covered for 2026. Avoiding coverage can lead to significant financial risk in case of illness or injury.

- Individuals with Marketplace Plans: Even if you’re currently enrolled in a plan through the Marketplace, it’s crucial to review your options. Plans change annually – premiums, deductibles, co-pays, and even the network of doctors and hospitals can be altered. Your current plan might not be the best fit for 2026, or a new, more affordable option might be available.

- Individuals Losing Employer-Sponsored Coverage: If you anticipate losing job-based coverage in the near future or by the end of the year, the OEP is a vital time to secure alternative coverage. While losing job-based coverage often qualifies you for a Special Enrollment Period, utilizing the OEP ensures you have options and avoids potential gaps.

- Individuals Seeking Different Coverage: Maybe your healthcare needs have changed, or you’re dissatisfied with your current plan’s benefits or costs. The OEP allows you to switch to a plan that better aligns with your current situation.

- Individuals Who Qualify for Subsidies: Many people are eligible for financial assistance (subsidies) to help lower their monthly premiums and out-of-pocket costs. These subsidies are only available for plans purchased through the Health Insurance Marketplace.

Navigating Your Options: Types of Health Insurance Plans

Understanding the different types of health plans available is a critical step in making an informed decision during the 2026 Open Enrollment. Each plan type comes with its own structure, benefits, and limitations:

- HMO (Health Maintenance Organization): Generally offers lower monthly premiums but requires you to choose a primary care physician (PCP) within the plan’s network. Your PCP then refers you to specialists. Out-of-network care is usually not covered, except in emergencies.

- PPO (Preferred Provider Organization): Provides more flexibility than an HMO. You don’t typically need a referral to see a specialist, and you can see out-of-network providers, though at a higher cost. Premiums are often higher than HMOs.

- EPO (Exclusive Provider Organization): A hybrid of HMO and PPO. You don’t need a referral for specialists, but you must stay within the plan’s network for covered care (except for emergencies).

- POS (Point of Service): Similar to an HMO in that you choose a PCP, but you can go out of network for care, though you’ll pay more. Referrals might be needed for specialists, even within the network.

- HDHP (High Deductible Health Plan) with HSA (Health Savings Account): These plans have higher deductibles but lower monthly premiums. They can be paired with an HSA, a tax-advantaged savings account used for healthcare expenses. HSAs are a great option for those who are generally healthy and want to save for future medical costs.

Consider your personal healthcare needs, your desired level of flexibility, and your budget when evaluating these different plan structures for the 2026 Open Enrollment.

Comparing Plans and Costs: What to Look For

Once you understand the plan types, the next step is to meticulously compare plans. Don’t just look at the monthly premium. A truly cost-effective plan considers the full financial picture:

- Monthly Premiums: This is the amount you pay each month for coverage.

- Deductible: The amount you must pay out-of-pocket for covered services before your insurance plan starts to pay. High deductibles often mean lower premiums, and vice-versa.

- Copayments (Copays): A fixed amount you pay for a covered health service after you’ve paid your deductible.

- Coinsurance: Your share of the cost for a covered health service, calculated as a percentage (e.g., 20%) of the allowed amount for the service, after you’ve paid your deductible.

- Out-of-Pocket Maximum: The most you have to pay for covered services in a plan year. After you reach this amount, your health plan pays 100% of the costs for covered benefits. This is a critical figure for financial protection against catastrophic illness.

- Provider Network: Ensure your preferred doctors, specialists, and hospitals are included in the plan’s network. Out-of-network care can be significantly more expensive or not covered at all.

- Prescription Drug Coverage: Check the plan’s formulary (list of covered drugs) to ensure your essential medications are included and understand their cost tiers.

- Benefits and Services: Review what services are covered, including preventive care, mental health services, maternity care, and rehabilitation.

The Health Insurance Marketplace (Healthcare.gov) and state-based exchanges offer tools to compare plans side-by-side, making it easier to evaluate these factors. Remember, the cheapest premium isn’t always the best value if it comes with high deductibles and limited benefits that don’t meet your needs. Be mindful of the 2026 Health Enrollment Deadline as you conduct your comparisons.

Financial Assistance: Are You Eligible for Subsidies?

One of the most significant advantages of enrolling through the Health Insurance Marketplace is the availability of financial assistance, often referred to as subsidies. These subsidies can significantly reduce the cost of health insurance, making coverage more affordable for millions of Americans.

- Premium Tax Credits (APTC): These credits lower your monthly health insurance premium. Eligibility is based on your household income and family size. Many people who thought they earned too much in the past may now qualify due to legislative changes.

- Cost-Sharing Reductions (CSRs): These subsidies help lower your out-of-pocket costs, such as deductibles, copayments, and coinsurance. CSRs are available only if you enroll in a Silver-level plan and meet specific income requirements.

When you apply for coverage through Healthcare.gov or your state’s exchange, you’ll provide income and household information, and the system will automatically determine your eligibility for these subsidies. It’s crucial to provide accurate information to ensure you receive all the financial help you’re entitled to. Don’t let perceived high costs deter you from exploring your options during the 2026 Open Enrollment Period.

Steps to Take Before the December 15th Deadline

To ensure a smooth enrollment process and meet the December 15th deadline, follow these steps:

- Gather Your Information: You’ll need personal information for everyone in your household, including Social Security Numbers, employer and income information (pay stubs, W-2s, tax returns), and current health insurance policy numbers if applicable.

- Estimate Your 2026 Income: Your eligibility for financial assistance is based on your estimated Modified Adjusted Gross Income (MAGI) for 2026. Be as accurate as possible.

- Review Your Current Plan (if applicable): If you have a Marketplace plan, review any notices from your current insurer about changes for 2026. Your plan might be automatically re-enrolled, but it’s often not the best option.

- Visit Healthcare.gov or Your State Exchange: This is the primary portal for comparing plans and applying for subsidies. Create an account or log in to your existing one.

- Compare Plans Carefully: Use the comparison tools to evaluate premiums, deductibles, out-of-pocket maximums, networks, and benefits.

- Seek Assistance if Needed: If you find the process overwhelming, free help is available. Navigators, certified application counselors, and licensed insurance agents can provide unbiased guidance. These resources can be found on Healthcare.gov or your state exchange website.

- Enroll by December 15th: Once you’ve chosen a plan, complete your application and enroll by the 2026 Health Enrollment Deadline of December 15th for coverage to start on January 1, 2026.

Special Considerations and Common Pitfalls to Avoid

Automatic Re-enrollment

If you’re currently enrolled in a Marketplace plan and do nothing, you may be automatically re-enrolled into your current plan or a similar one for 2026. While this might seem convenient, it’s rarely the best option. Your premium might increase, your benefits could change, or a more affordable or suitable plan might become available. Always actively review and choose a plan for the upcoming year.

Understanding Plan Metal Tiers (Bronze, Silver, Gold, Platinum)

Marketplace plans are categorized into metal tiers based on how costs are split between you and your insurance company:

- Bronze: Low monthly premiums, high deductibles. Covers about 60% of costs. Best for people who expect to use healthcare services sparingly.

- Silver: Moderate monthly premiums and deductibles. Covers about 70% of costs. Only tier eligible for Cost-Sharing Reductions. Good for those who qualify for subsidies and use healthcare services moderately.

- Gold: High monthly premiums, low deductibles. Covers about 80% of costs. Best for people who expect to use a lot of healthcare services.

- Platinum: Highest monthly premiums, lowest deductibles. Covers about 90% of costs. Ideal for those with extensive healthcare needs.

Choosing the right metal tier requires balancing your expected healthcare usage with your budget. The 2026 Open Enrollment Period is your chance to make this strategic decision.

Short-Term Health Insurance Plans

Be wary of short-term health insurance plans. While they often have lower premiums, they typically offer very limited benefits, don’t cover pre-existing conditions, and are not compliant with the Affordable Care Act (ACA). They are not a substitute for comprehensive health insurance and should only be considered as a temporary bridge in specific circumstances, never as a long-term solution during the 2026 Open Enrollment.

What Happens if You Miss the 2026 Health Enrollment Deadline?

Missing the final enrollment deadline (typically January 15, 2026, for federal marketplaces) means you generally cannot enroll in a health insurance plan through the Marketplace until the next Open Enrollment Period, unless you qualify for a Special Enrollment Period (SEP). This could leave you uninsured for most of 2026, exposing you to significant financial risk for medical expenses. Avoid this scenario by prioritizing the December 15th deadline and subsequent final deadline.

Even if you miss the December 15th deadline for January 1st coverage, remember you still have until the final OEP deadline (usually January 15th) to enroll for February 1st coverage. However, aim for the earlier date to ensure continuous protection.

The Role of the Affordable Care Act (ACA) in 2026 Open Enrollment

The Affordable Care Act (ACA) continues to be the bedrock of the Health Insurance Marketplace. It ensures that health insurance plans offered through the Marketplace cover essential health benefits, cannot deny coverage based on pre-existing conditions, and place no annual or lifetime limits on essential health benefits. The ACA also underpins the financial assistance programs (premium tax credits and cost-sharing reductions) that make coverage affordable for millions.

Understanding the protections and benefits afforded by the ACA is crucial as you navigate the 2026 Open Enrollment. It ensures a baseline level of comprehensive coverage and consumer protection that might not be present in non-ACA compliant plans.

Preparing for Your Enrollment Conversation with an Expert

If you plan to seek assistance from a Navigator, certified application counselor, or licensed insurance agent, preparing in advance can make your consultation more productive. Have your income documents ready, a list of your preferred doctors and medications, and any questions you have about specific plan features. These experts are invaluable resources, especially when facing the 2026 Health Enrollment Deadline.

Conclusion: Act Now for Your 2026 Health Coverage

The 2026 Open Enrollment Period is a vital opportunity to secure or update your health insurance. With the crucial December 15th deadline fast approaching for new plans starting January 1st, procrastination is not an option. Take the time now to research your options, understand the different plan types, compare costs and benefits, and determine your eligibility for financial assistance. Utilize the resources available through Healthcare.gov, state exchanges, and local assistance programs.

Don’t leave your health and financial security to chance. By acting proactively and meeting the 2026 Health Enrollment Deadline, you can ensure you have comprehensive, affordable health coverage in place for the year ahead, providing invaluable peace of mind. Mark your calendar, gather your information, and make an informed decision to protect what matters most.