2026 FAFSA Changes: Your Guide to Federal Student Aid Updates and Deadlines

Anúncios

The journey to higher education in the United States is often accompanied by the significant hurdle of financing. For millions of students and their families, the Free Application for Federal Student Aid (FAFSA) is the gateway to unlocking crucial financial assistance. As we look towards the 2026 academic year, it’s imperative for prospective college students and their guardians to understand the evolving landscape of federal student aid. The Department of Education continually refines its processes and policies, and the 2026 FAFSA Changes are set to bring notable adjustments that could impact eligibility, award amounts, and the overall application experience. This comprehensive guide aims to demystify these updates, providing you with the knowledge and strategies needed to navigate the application process successfully.

Understanding the FAFSA is not merely about filling out a form; it’s about strategizing to maximize your financial aid potential. The information you provide on the FAFSA is used to determine your Student Aid Index (SAI), formerly known as the Expected Family Contribution (EFC), which is a key factor in calculating your eligibility for various types of federal, state, and institutional aid. Therefore, staying informed about the latest 2026 FAFSA Changes is not just recommended, it’s essential for anyone planning to attend college in the coming years.

Anúncios

The Evolution of FAFSA: Why Changes Are Constant

The FAFSA is not a static document; it undergoes periodic revisions to adapt to economic shifts, legislative mandates, and efforts to streamline the application process. These changes are often aimed at making federal student aid more accessible, equitable, and easier to understand for all applicants. The most significant overhaul in recent memory came with the FAFSA Simplification Act, which began implementation for the 2024-2025 aid year and continues to influence subsequent cycles, including the 2026 FAFSA. These legislative efforts seek to improve the student aid experience by simplifying the application, expanding eligibility for federal student aid, and providing a more accurate assessment of a student’s financial need.

The reasons behind these constant evolutions are multifaceted. Economic indicators, such as inflation and employment rates, play a role in how aid formulas are adjusted. Furthermore, feedback from students, families, financial aid administrators, and advocacy groups also contributes to the refinement of the FAFSA process. The goal is always to create a system that is fair, transparent, and effective in helping students achieve their educational aspirations without being unduly burdened by financial constraints. Therefore, approaching the 2026 FAFSA Changes with an open mind and a commitment to understanding the new rules will be crucial for prospective applicants.

Anúncios

Key 2026 FAFSA Changes to Anticipate

While the full scope of all 2026 FAFSA Changes may not be entirely finalized until closer to the application launch, certain trends and confirmed adjustments from recent simplification efforts provide a strong indication of what to expect. Here are some of the most impactful changes to keep on your radar:

1. The Student Aid Index (SAI) Replaces the EFC

One of the most significant shifts introduced by the FAFSA Simplification Act, and continuing into 2026, is the replacement of the Expected Family Contribution (EFC) with the Student Aid Index (SAI). While both are indices used to determine aid eligibility, the SAI calculation is designed to be a more accurate and equitable measure of a student’s ability to pay for college. Key differences include:

- No Negative SAI: Unlike the EFC, which could be as low as zero, the SAI can be a negative number (down to -1500). A negative SAI indicates a higher level of financial need, potentially leading to increased Pell Grant eligibility.

- Changes to Family Size: The new methodology uses federal tax information (FTI) directly transferred from the IRS to determine family size, which can impact aid calculations. This change aims to simplify the process and reduce errors.

- Exclusion of Small Business and Farm Net Worth: For some applicants, the net worth of small businesses and family farms that they own and control will be excluded from the asset calculation, which could significantly lower their SAI and increase aid eligibility.

- Child Support Treatment: Child support received will now be reported as an asset, not as untaxed income, which may affect some families’ SAI.

2. Streamlined Application Process

The FAFSA form itself has been simplified, reducing the number of questions and making the application more user-friendly. This is a continuous effort, and applicants for 2026 can expect a more intuitive experience. The main goal is to make the application process less daunting, encouraging more students to apply for federal aid.

3. Direct Data Exchange with the IRS

A major feature of the simplified FAFSA is the mandatory use of the Direct Data Exchange (DDX) with the IRS. This allows for direct transfer of tax information into the FAFSA, significantly reducing the burden on applicants to manually input tax data and minimizing errors. All contributors (student, spouse, parents, etc.) will need to provide consent for their tax data to be transferred. Without this consent, the student will not be eligible for federal student aid.

4. Expanded Pell Grant Eligibility

The FAFSA Simplification Act aims to expand Pell Grant eligibility, particularly for students from low-income backgrounds. The new SAI calculation and the automatic qualification for Pell Grants based on federal poverty levels and family size are key components of this expansion. For the 2026 FAFSA, more students may find themselves eligible for Pell Grants or for larger award amounts.

5. Changes for Divorced or Separated Parents

The rule for which parent’s information to report on the FAFSA has changed. Instead of determining the custodial parent based on who provides more financial support, the FAFSA will now require information from the parent who provides the greater portion of the student’s financial support, or the parent who lives with the student more than 50% of the time, regardless of who claims them on their taxes. This aims to simplify a historically confusing aspect of the application.

New Deadlines and Application Timeline for 2026

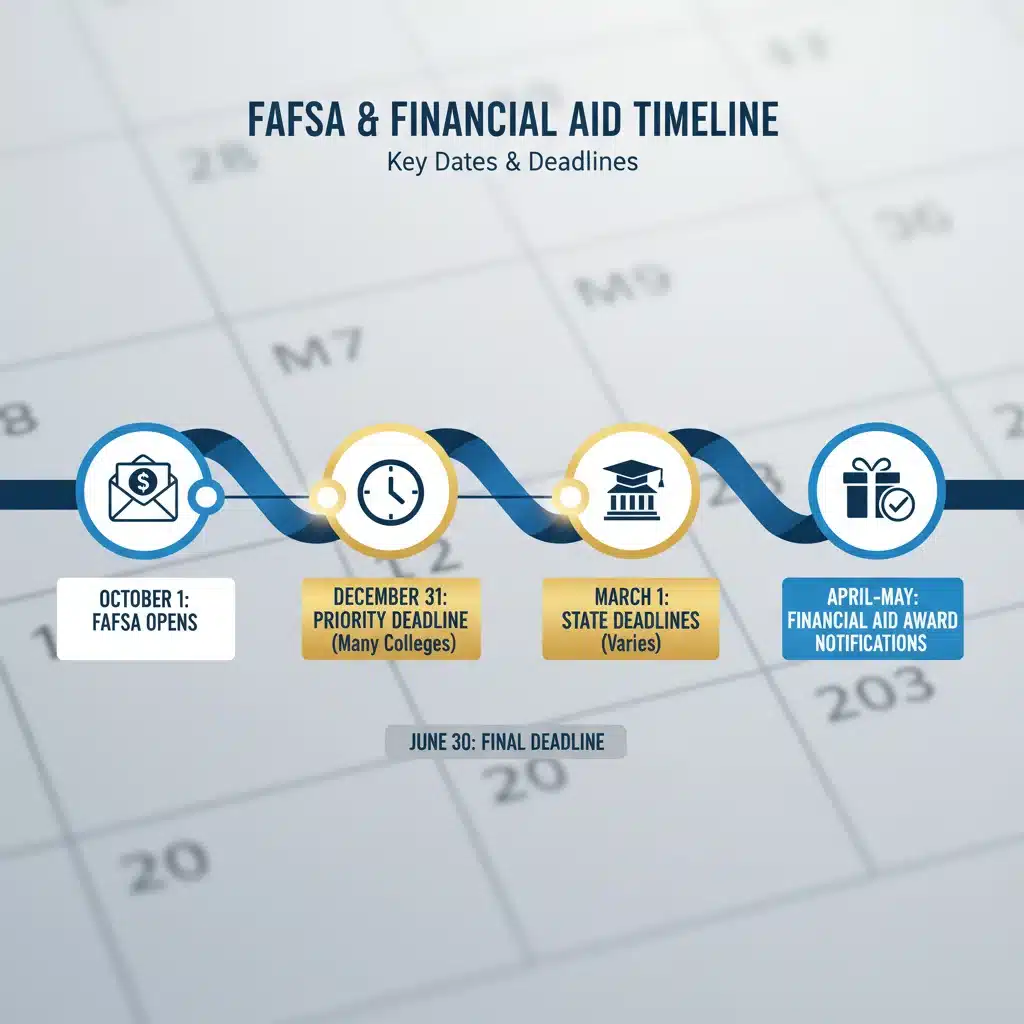

While the exact opening date for the 2026-2027 FAFSA will be announced by the Department of Education, it traditionally opens on October 1st of the year prior to the academic year for which you are seeking aid. However, with the recent FAFSA Simplification Act, there have been some adjustments and potential delays in the past. It is crucial to monitor official announcements from Federal Student Aid (studentaid.gov) for the precise opening date for the 2026 FAFSA.

- Federal Deadline: The federal deadline for submitting the FAFSA is typically in June of the academic aid year. For the 2026-2027 academic year, this would likely be June 30, 2027. However, this deadline is often much later than institutional and state deadlines.

- State Deadlines: Many states have their own FAFSA deadlines, which can be as early as January or February. Missing a state deadline could mean missing out on state-specific grants and scholarships.

- Institutional Deadlines: Colleges and universities also set their own priority deadlines, often in conjunction with application deadlines for admissions or scholarships. Submitting your FAFSA by these priority deadlines is critical, as aid funds are often limited and distributed on a first-come, first-served basis.

Pro-Tip: Always check the specific deadlines for each college you are applying to, as well as your state’s financial aid agency website. Do not rely solely on the federal deadline, as it is often too late to qualify for many aid programs.

Who Are the "Contributors" and What Do They Need to Do?

With the updated FAFSA, the concept of "contributors" is more pronounced. Contributors are anyone who is required to provide information and consent for the FAFSA, which typically includes the student, their spouse (if applicable), and one or both parents (if the student is dependent). Each contributor will need to have their own Federal Student Aid (FSA) ID and provide consent for their tax data to be transferred directly from the IRS via the Direct Data Exchange (DDX).

Key Contributor Responsibilities:

- Obtain an FSA ID: Every contributor must have a verified FSA ID. This serves as your electronic signature and allows you to access and sign the FAFSA. It’s recommended to create this well in advance of the application opening.

- Provide Consent: All contributors must provide consent for the IRS to share their tax information. Without this consent, the FAFSA cannot be processed, and the student will not be eligible for federal aid.

- Review Information: Even with direct data exchange, it’s crucial for contributors to review all information for accuracy before submitting the FAFSA.

Strategies for Navigating the 2026 FAFSA Changes

Given the upcoming 2026 FAFSA Changes, a proactive and informed approach is vital for success. Here are some strategies to help you navigate the process effectively:

1. Stay Informed and Monitor Official Sources

The most important strategy is to continuously monitor official sources for updates. The Federal Student Aid website (studentaid.gov) is your primary resource. Sign up for email alerts and follow their social media channels for real-time announcements regarding the 2026 FAFSA opening, deadlines, and any further clarifications on policy changes.

2. Create Your FSA ID Early

Do not wait until the last minute to create your FSA ID. Both the student and any required parent contributors need an FSA ID. The process involves verifying your identity, which can take a few days. Having this ready ensures you can access and sign the FAFSA as soon as it opens.

3. Gather Necessary Documents in Advance

Although the Direct Data Exchange simplifies tax information transfer, you’ll still need other documents. These typically include:

- Social Security numbers for the student and parents.

- Driver’s license number (if you have one).

- Alien Registration Number (if you are not a U.S. citizen).

- Records of untaxed income (e.g., child support received, interest income, veterans’ non-education benefits).

- Information on cash, savings, checking account balances, investments (excluding retirement accounts), and real estate (excluding the family home).

4. Understand the New SAI Calculation

Familiarize yourself with how the Student Aid Index (SAI) is calculated. While you don’t need to be an expert, understanding which financial factors influence your SAI can help you anticipate your aid eligibility and make informed financial decisions. Resources on studentaid.gov and your college’s financial aid office can provide detailed explanations.

5. Prioritize Early Submission

Even with a streamlined process, submitting your FAFSA as early as possible is always beneficial. Many states and colleges award aid on a first-come, first-served basis, meaning that waiting could reduce the amount of aid you receive, even if you are eligible. Aim to complete and submit your FAFSA shortly after it opens.

6. Seek Assistance When Needed

Don’t hesitate to reach out for help. College financial aid offices are excellent resources for understanding the FAFSA and institutional aid. You can also contact Federal Student Aid directly through their help center or by phone if you encounter specific issues with the application.

Impact on Different Student Populations

The 2026 FAFSA Changes are designed to positively impact various student populations, though the degree of impact may vary.

Low-Income Students

The expanded Pell Grant eligibility and the possibility of a negative SAI are particularly beneficial for low-income students, potentially increasing their access to federal grants that do not need to be repaid. The simplified application process also aims to reduce barriers for these students, who may have fewer resources to navigate complex forms.

Students with Divorced or Separated Parents

The revised rules for reporting parental information could simplify the process for students whose parents are divorced or separated, reducing confusion and potential errors that previously caused delays or incorrect aid calculations.

Small Business Owners and Farmers

The exclusion of small business and family farm net worth from asset calculations can significantly benefit families who derive their income from these sources, potentially lowering their SAI and increasing their aid eligibility.

Undocumented Students and DACA Recipients

It’s important to note that while federal student aid is generally limited to U.S. citizens and eligible non-citizens, some states offer their own financial aid programs that may be accessible to undocumented students or DACA recipients. These students should research state-specific aid opportunities and institutional policies, as the federal FAFSA changes do not directly alter their federal eligibility.

Beyond FAFSA: Other Avenues for Financial Aid

While the FAFSA is the cornerstone of federal student aid, it’s just one piece of the financial aid puzzle. Students should also explore other funding opportunities:

1. Scholarships

Scholarships are funds that do not need to be repaid and are awarded based on various criteria, such as academic merit, athletic talent, community service, specific majors, or demographic factors. There are countless scholarship opportunities available from colleges, private organizations, and foundations. Start your scholarship search early and apply to as many as you qualify for.

2. Grants

In addition to federal Pell Grants, many states and individual colleges offer their own grant programs. These are typically need-based and do not need to be repaid. Check with your state’s higher education agency and the financial aid offices of the colleges you are interested in.

3. Institutional Aid

Colleges and universities often provide their own institutional grants and scholarships, sometimes based on financial need, academic merit, or a combination of both. Some private institutions may also require the CSS Profile, a separate financial aid application, in addition to the FAFSA, to determine eligibility for their own funds.

4. Work-Study Programs

Federal Work-Study provides part-time jobs for undergraduate and graduate students with financial need, allowing them to earn money to help pay for educational expenses. The earnings do not count against you in future FAFSA calculations, which is a significant advantage.

5. Private Student Loans

After exhausting all federal, state, and institutional aid options, some students may consider private student loans. These are offered by banks, credit unions, and other private lenders. It’s crucial to understand that private loans typically have higher interest rates and fewer borrower protections than federal loans, so they should be a last resort.

Common Misconceptions About FAFSA

Despite its importance, several misconceptions about the FAFSA persist. Addressing these can help you avoid costly mistakes:

- "My parents make too much money." This is one of the most common myths. Many factors beyond income go into the SAI calculation, including family size, number of children in college, and certain assets. You might be surprised at what you qualify for. Always apply!

- "I’m only going to apply for scholarships, so I don’t need FAFSA." Many scholarships, even those based on merit, require a completed FAFSA to assess financial need or as a general eligibility requirement.

- "Only students with good grades get financial aid." While merit-based aid exists, federal student aid is primarily need-based. Your grades do not directly impact your eligibility for federal grants or loans.

- "FAFSA is only for federal grants and loans." The FAFSA is also used by states and colleges to determine eligibility for their own financial aid programs.

- "I’m too old for financial aid." There is no age limit for federal student aid for undergraduate or graduate studies.

The Importance of Financial Literacy in College Planning

Beyond understanding the 2026 FAFSA Changes, developing strong financial literacy skills is paramount for college-bound students and their families. This includes:

- Budgeting: Learning to create and stick to a budget can help manage college expenses, from tuition and fees to living costs and personal spending.

- Understanding Loan Terms: If you do take out student loans, thoroughly understand the interest rates, repayment terms, and potential impact on your future finances.

- Saving for College: Exploring savings vehicles like 529 plans can significantly reduce the amount you need to borrow.

- Comparing Aid Packages: When you receive financial aid award letters from different colleges, learn how to compare them effectively to determine the true cost of attendance at each institution. Focus on the "net price" (cost of attendance minus grants and scholarships) rather than the sticker price.

Final Thoughts: Preparing for Your College Future

The 2026 FAFSA Changes represent an ongoing effort to simplify and improve the federal student aid system. While any change can bring a degree of uncertainty, the underlying goal remains the same: to help students afford higher education. By staying informed, preparing diligently, and utilizing all available resources, you can confidently navigate the financial aid process and secure the funding necessary to achieve your academic dreams.

Remember, the path to college is a significant investment, and understanding the nuances of financial aid is a critical component of that investment. Begin your research early, mark your calendars for important deadlines, and don’t hesitate to ask for help. Your future education is worth the effort.